")

")

[ad_1]

There was once rampant hypothesis after the Federal Open Marketplace Committee (FOMC) assembly final week concerning the timing and choice of rate of interest cuts this yr. In a follow-up interview on 60 Mins on Sunday, Federal Reserve Chairman Jerome Powell didn’t sound like any individual who has pivoted.

In reality, Powell believes the Fed can wait till it sees extra exertions injury ahead of reducing the Federal Budget Price aggressively or transferring towards a impartial coverage stance, announcing once more {that a} March fee lower is “not going.”

In December, the Fed mentioned 3 fee cuts in 2024 however some other folks made a case for 4, 5 and even six fee cuts given a Fed pivot. Alternatively, for me it’s at all times been concerning the exertions marketplace and jobless claims knowledge, and that knowledge line hasn’t damaged sufficient for the Fed to be extra competitive. For the Fed to lower charges in March, we would wish weaker exertions knowledge, regardless of how low inflation is going within the subsequent document.

Right here’s a part of the interview on 60 Mins that illustrates what I’m speaking about:

Scott Pelley: However inflation has been falling often for 11 months. You’ve have shyed away from a recession. Why no longer lower the charges now?

Jerome Powell: Smartly, we’ve a robust economic system. Enlargement is happening at a forged tempo, the exertions marketplace is powerful, 3.7% unemployment. With the economic system robust like that, we really feel like we will be able to manner the query of when to start to scale back rates of interest moderately. We need to see extra proof that inflation is transferring sustainably down to two%. Now we have some self assurance in that, our self assurance is emerging. We simply need some extra self assurance ahead of we take that essential step of starting to lower rates of interest.

Realize the remark, “We really feel like we will be able to manner the query of when to start to scale back rates of interest moderately.” That is the outdated and gradual section I’ve been discussing because the finish of 2022. The Fed already has a restrictive coverage and if the exertions marketplace was once breaking nowadays they’d be reducing charges aggressively. Alternatively, as an alternative of having forward of the curve and getting out of restrictive territory into impartial coverage, they’re going to take their time in this and keep restrictive for just a little longer.

This has been a theme of my paintings since 2022 and is why I want exertions knowledge over inflation knowledge at this degree. Again in 2022, the Fed mentioned having the Fed Budget fee replicate 3, six and 12-month PCE knowledge. As of late, PCE three-month and six-month inflation is operating under 2%, headline 12-month PCE is operating at 2.6%, core PCE 12-month is operating at 2.9% and the Fed finances fee is over 5%.

With that more or less growth in inflation, why is the Fed risking being restrictive with its coverage? It’s as a result of they’re going to really feel higher about reducing charges when the exertions marketplace is breaking. The knowledge line that may alternate the entirety isn’t extra BLS jobs Friday studies like we simply had, however the jobless claims knowledge. It is just too low for the Fed to pivot.

We are going to peer fee cuts this yr. The Fed believed that coverage was once too restrictive when the 10-year was once close to 5% and we had 8% loan charges, however they appear superb with loan charges between 6%-7.25% at this time. Right here’s every other quote from the 60 Mins interview:

Pelley: The following assembly round this desk that may make a decision the course of rates of interest is on this coming March. Understanding what you already know now, is a fee lower much more likely or much less most probably at the moment?

Powell: So, the wider scenario is that the economic system is powerful, the exertions marketplace is powerful, and inflation is coming down. And my colleagues and I try to pick out the correct level at which to start to dial again our restrictive coverage stance.

This obviously displays that the Fed hasn’t pivoted now, they simply didn’t need their coverage to be too restrictive. The very last thing they would like on their plate is a job-loss recession going into an election yr once they hiked so prime so speedy.

Bond yields react

Let’s take a primary look on the bond marketplace response to the interview. The ten-year yield headed upper after this interview went are living, emerging from 4.02% to 4.07%.

The ten-year yield is the important thing for housing in 2024. In my 2024 forecast, I set the 10-year yield vary between 3.21%-4.25%, with a crucial line within the sand at 3.37%. If the industrial knowledge remains company, we shouldn’t ruin under 3.21%, but when the exertions knowledge will get weaker, that line within the sand — which I name the Gandalf line, as in “you shall no longer move” — shall be examined.

This 10-year yield vary manner loan charges between 5.75%-7.25%, however this assumes spreads are nonetheless unhealthy. The spreads had been bettering this yr such a lot that if we hit 4.25% at the 10-year yield, we received’t see 7.25% in loan charges.

Underneath is the chart of the 10-year yield since Feb. 1 and you’ll see the response after Powell talked on 60 mins Sunday: yields went upper.

We’re within the upper-end vary of my 10-year yield forecast, and jobless claims are close to the ancient backside of the post-COVID-19 restoration. My fashion is primarily based extra on claims knowledge, so this seems about proper.

What about housing?

Powell didn’t speak about housing in any respect on this interview and the Fed is in a type of no-man’s land when speaking about housing. The one silver lining I will say right here for the housing marketplace is if the Fed didn’t discuss a 5% 10-year yield and eight% loan charges being too restrictive with Fed coverage. We may well be there nowadays after the final jobs document! That’s essentially the most sure spin I will take from the new movements — that they know they had been pushing the bounds with the housing marketplace.

Keep in mind, maximum recessions get started with shedding residential building jobs in order that they’re conscious of this truth in an election yr.

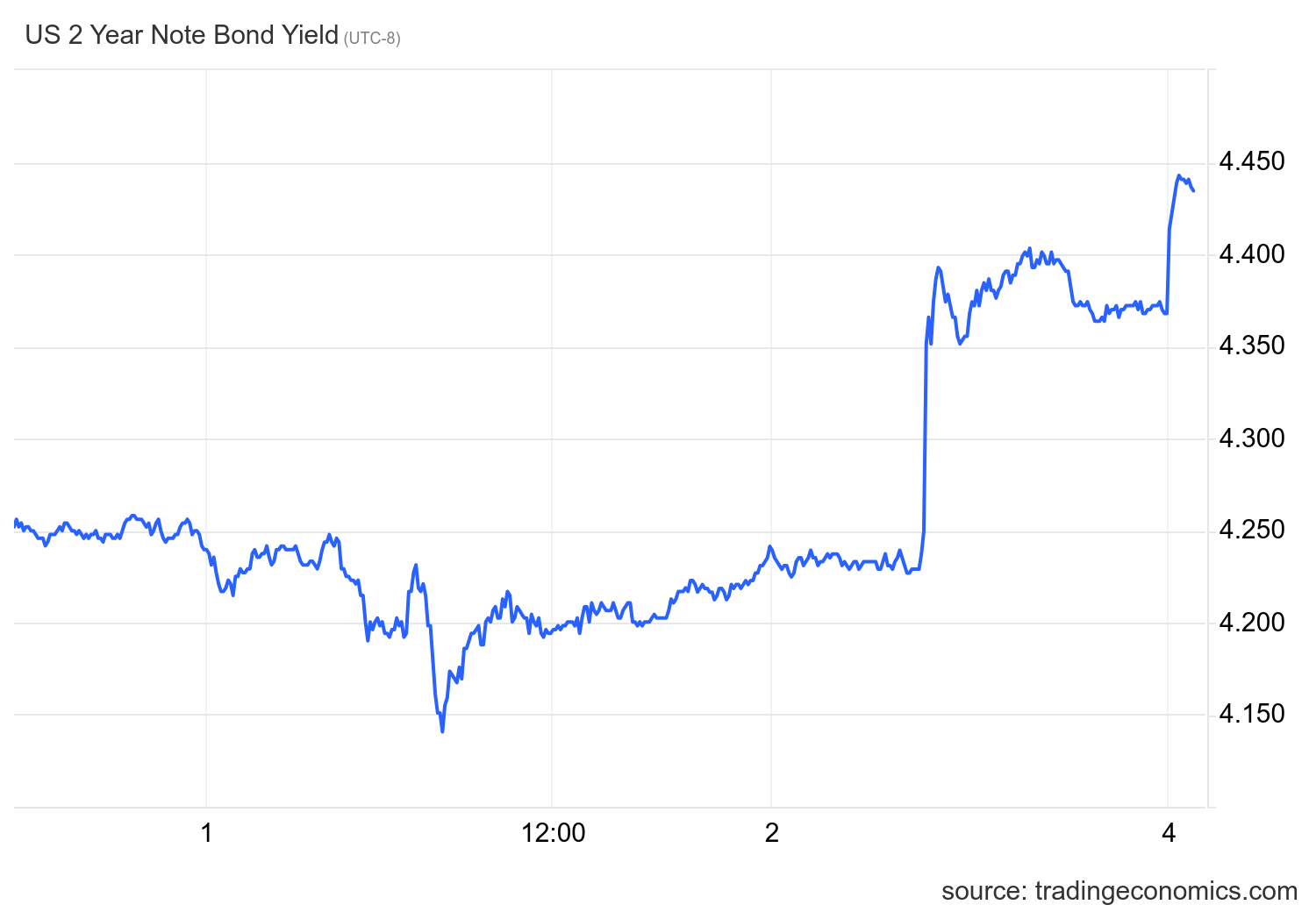

At this level of the cycle, if you wish to have an concept on fee cuts, the 2-year yield is the most productive position to move. I can stand company on getting not more than 3 fee cuts in 2024 except jobless claims get to 323,000 on a four-week transferring moderate. Sadly, if the Fed hasn’t pivoted by way of then it’s going to be too past due. At this time, the 2-year yield is emerging from fresh lows, making extra competitive fee lower forecasts not going.

Just like the 10-year, the chart of the 2-year yield under displays a robust response to the 60 Mins interview.

Powell’s newest interview makes it transparent: Not anything large will alternate over the following few months it doesn’t matter what occurs with inflation — the exertions marketplace hasn’t damaged sufficient for the Federal Reserve to pivot.

Comparable

[ad_2]