[ad_1]

Housing call for is up and it’s time to trace the spring housing information and spot what the marketing season will convey. As I at all times pressure, we’re running from the bottom bar ever with call for, so let’s upload historic context to the information. However, even with loan charges upper this yr than ultimate yr, call for is emerging.

Acquire software information

As we get nearer to the top of the primary month of 2024, forward-looking acquire software information appears excellent. After I make some vacation changes, now we have 8 weeks of a favorable pattern since loan charges fell from the 8% top, and as of now, the rather upper charges we’ve observed not too long ago haven’t impacted the information simply but. Traditionally, upper charges negatively affect the weekly acquire software information, and I will be able to search for this over the following few weeks . But it surely’s very early within the seasonal call for time-frame for housing, so we will be able to take it one week at a time. Acquire apps had been up 8% week to week and nonetheless down 18% yr over yr. Remaining yr right now we were given a spice up in call for with charges heading towards 6%.

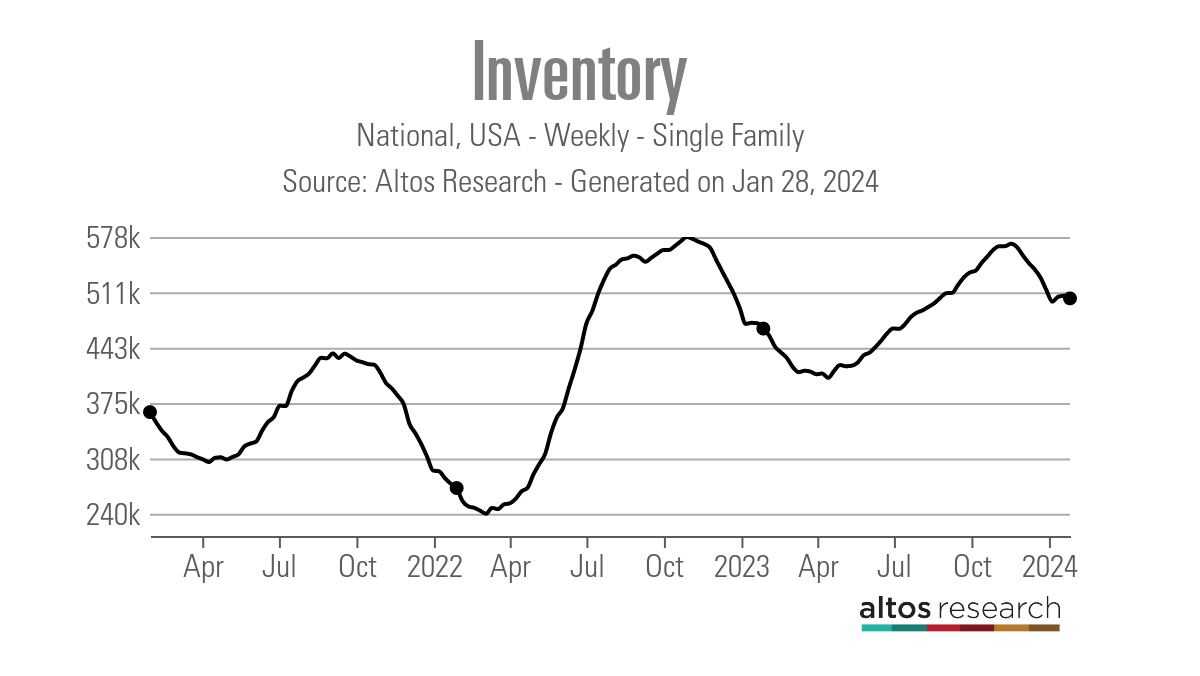

Weekly housing stock information

Here’s a take a look at ultimate week:

- Weekly stock alternate (Jan. 19-26): Stock fell from 506,414 to 503,233

- Similar week ultimate yr (Jan. 20-27): Stock fell from 472,852 to 466,391

- The stock backside for 2022 was once 240,194

- The stock height for 2023 is 569,898

- For context, lively listings for this week in 2015 had been 938,453

Remaining week, we noticed lively stock fall rather week to week. That is not unusual in January. We’ve had some certain acquire software information not too long ago, and the pending house gross sales file got here in as a beat ultimate week. So, stock falling appears standard. Alternatively, I want to see the stock backside very quickly and feature a extra conventional seasonal building up, reasonably than having a backside in March or April.

New listings information

One of the crucial extra certain tales about housing stock not too long ago is that we discovered a backside in new listings information ultimate yr, and now we have been beginning to develop new listings information for a while now on a year-over-year foundation. It isn’t the rest important, however I will be able to take it after what now we have been thru the previous couple of years. That is one thing I mentioned on CNBC not too long ago.

Weekly new list information:

- 2024: 44,921

- 2023: 42,843

- 2022: 47,713

Worth reduce proportion

Once a year, one-third of all houses take a payment reduce ahead of promoting — not anything extraordinary about that. Alternatively, this knowledge line hurries up upper when loan charges upward push, and insist will get hit tougher. An ideal instance was once in 2022: when housing stock rose quicker, the proportion of payment cuts rose quicker as house gross sales crashed. That building up matched the slope of the stock building up, and folks had to reduce costs to promote their houses.

Towards the top of 2022, that market modified as house gross sales stopped crashing and the marketplace stabilized. To this point this yr, the value reduce proportion information remains to be on tempo to wreck beneath the lows we noticed in 2023 within the spring. This information line may be very seasonal, so what is going on now may be very standard.

That is the price-cut proportion for a similar week over the previous couple of years:

- 2024: 31.%

- 2023: 34.%

- 2022: 20.%

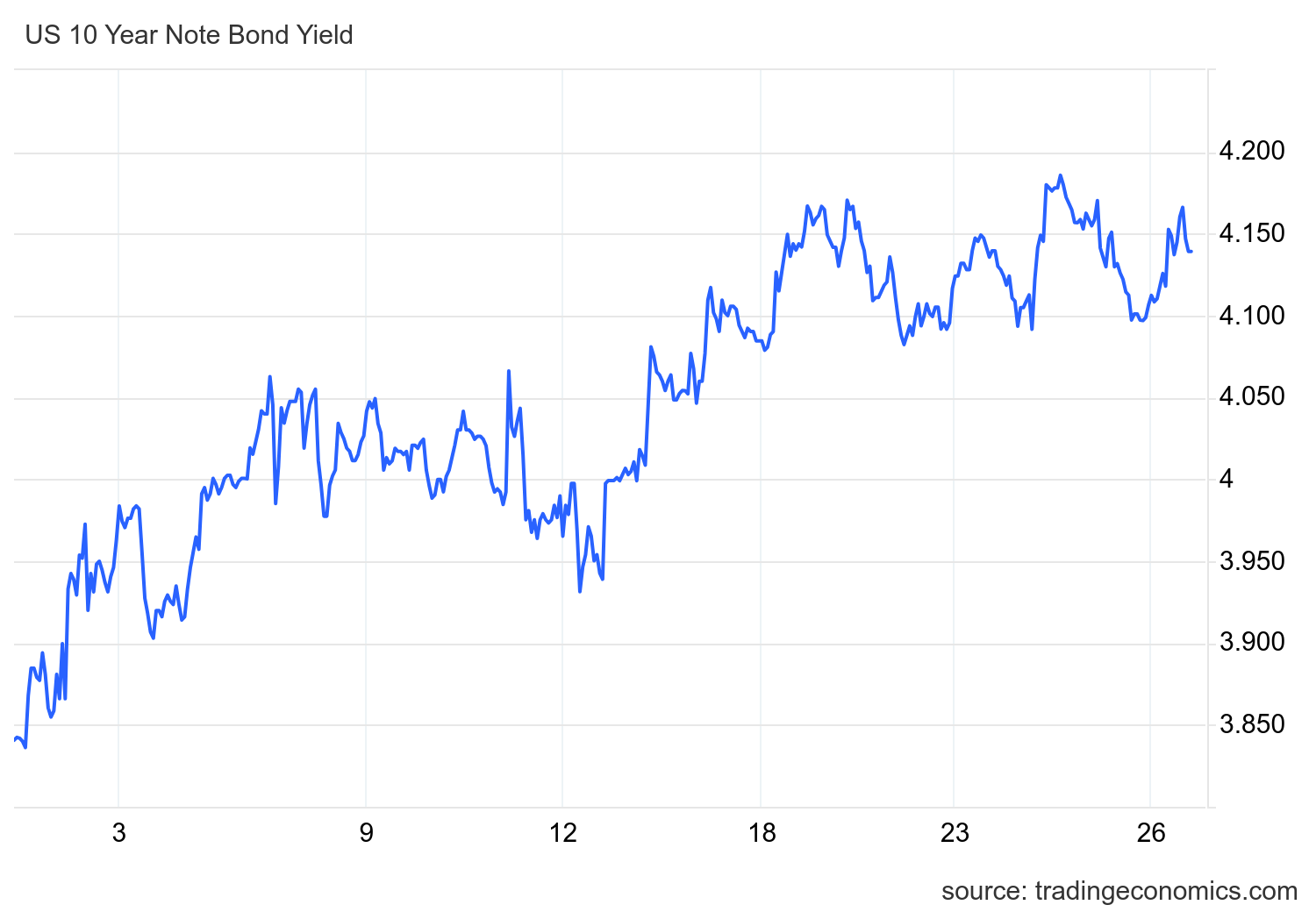

Loan charges and the 10-year yield

The ten-year yield is the important thing for housing in 2024. In my 2024 forecast, I’ve the 10-year yield vary between 3.21%-4.25%, with a crucial line within the sand at 3.37%. If the commercial information remains company, we shouldn’t destroy beneath 3.21%, but when the exertions information will get weaker, that line within the sand — which I name the Gandalf line, as in “you shall now not move” — will likely be examined.

This 10-year yield vary way loan charges between 5.75%-7.25%, however this assumes spreads are nonetheless unhealthy. The spreads had been making improvements to this yr such a lot that if we hit 4.25% at the 10-year yield, we received’t see 7.25% in loan charges.

Remaining week, we were given nice information on inflation information, and now we have been announcing the inflation enlargement fee has slowed. Alternatively, within the financial sport of rock-paper-scissors, it’s exertions over inflation information, and the jobless claims information are too low, so the Fed hasn’t pivoted but. Monday’s podcast will cross over this matter extra obviously.

The ten-year yield began ultimate week at 4.14% and ended the week there. Loan charges ranged between 6.875% and six.95%, finishing the week at 6.90%. There isn’t a lot motion with the 10-year yield and loan charges. It’s wild to suppose that 3 to 6 month PCE inflation information is operating beneath 2%, and loan charges are nonetheless this top. Keep in mind, the Fed hasn’t pivoted and remains to be very restrictive.

The week forward: Jobs, the Fed and residential costs

It’s jobs week! So we will be able to get the 4 exertions reviews: Activity openings, ADP, jobless claims and the BLS jobs file. The Federal Reserve meets this week: we received’t see a fee reduce this time however the secret’s the language they use on this assembly after the hot inflation information we noticed. Additionally, the query and solutions will have to be very fascinating. We even have some house payment information, which after all is just a little lagging from what is occurring these days, however we will be able to get the ones reviews as neatly.

Similar

[ad_2]