[ad_1]

I’ve been saving into Collection I bonds for rather a while however it wasn’t till the previous couple of years that we’ve noticed some eye-popping charges out of Collection I bonds.

I were given in at the fervor a couple of years in the past when inflation was once operating sizzling and we noticed Collection I bonds providing inflation charges of three.56%, 4.81%, and three.24%. In fact, they got here with mounted charges that had been 0.00% – however they nonetheless put Collection I bonds charges into the stratosphere.

However with inflation slowing down and inflation charges taking place, numerous the ones Collection I bonds now not game lofty rates of interest. (in case you have a zero% mounted charge bond, your present rate of interest is solely 2 instances the inflation charge)

The query now’s, given the penalty laws for Collection I Bonds, will have to you redeem them or cling them? Or redeem them and re-buy again in now that mounted charges are upper?

Desk of Contents

We will be able to being with a refresher of the withdrawal laws, then a take a look at how you’ll evaluate your explicit Collection I bonds, then a choice tree on what you will have to believe.

Collection I Bond Withdrawal Regulations Refresher

In short, let’s evaluate the Collection I bond withdrawal laws:

- You can not redeem your bond inside a yr of factor.

- Should you redeem your bond inside 5 years of factor, you lose the final 3 months of passion. It really works out to be the present calendar month you’re in and the final two. So in November, you lose November, October, and September.

- If it’s previous 5 years, you’ll redeem them with out penalty.

Sooner than you’ll redeem them, it’s important to evaluate them to peer what you’re ready to do and what they’re incomes.

That is the way you evaluate your bonds:

Learn how to Overview Your Collection I Bonds

Step one is to take a look at your present Collection I bonds and notice what they’re incomes.

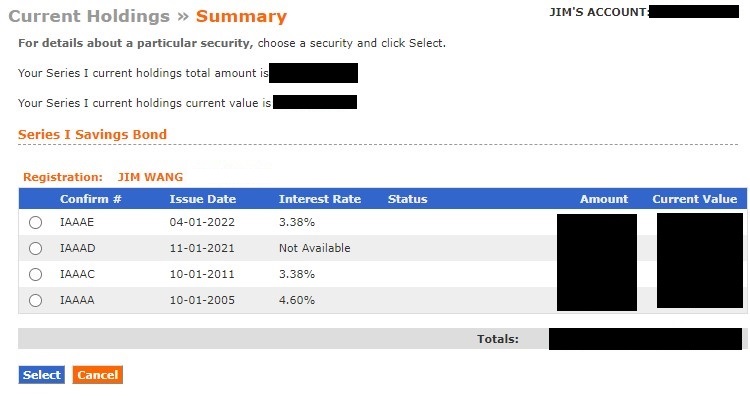

To do this, log into your Treasury Direct account and search for your bonds. My Financial savings Bonds are on the backside of the display:

Click on the circle to the left of the Collection I Financial savings Bond row and click on Put up.

As you’ll see, I’ve 4 Collection I Bonds that I will be able to redeem. All 4 are past the only yr withdrawal restriction however best two of them are past the 5 yr restriction.

The “Pastime Price” proven within the desk above is the calculated charge in accordance with the bond’s present inflation charge and its mounted charge, set at factor.

Sadly, there’s no method to see the breakdown of the speed into the ones two numbers. Should you click on at the circle and “Make a choice” the bond, it displays you mainly the similar data:

To understand the present rate of interest breakdown, it’s important to glance it up at the Collection I Bond web page.

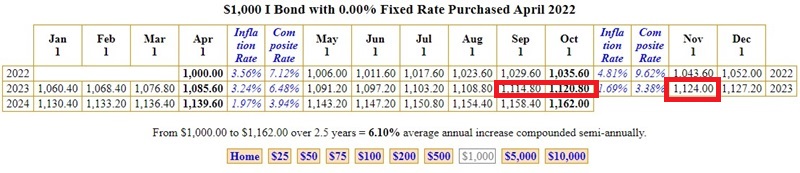

In accordance with the Factor Date of 10-01-2005, we have now a hard and fast charge of one.20%. The inflation charge lags as a result of a topic date of October 2005 manner we began with the Would possibly 2005 inflation charge for 6 months. This implies for October 2023, we’re taking a look on the Would possibly 2023 inflation charge for our inflation charge part.

Mounted charge of one.20% at the bond, 1.69% inflation charge for Would possibly 2023 = 4.60003%.

How A lot Pastime Do You Give Up?

You don’t need to need to calculate this for your entire bonds. Thankfully you don’t need to.

Whilst you take a look at your desk of Present Holdings, the “Present Worth” column is the worth of your bonds minus the passion you’d give up for early redemption. I blacked it out for mine for safety causes.

What if you wish to know in case you’re giving up “larger” passion bills? Most likely ready a month would assist?

There’s a web page Eyebonds.data that can display you precisely how a lot passion you are going to surrender. The Eyebonds web page displays you the worth of your bond in accordance with its factor date (and you’ll make a selection a bond price to assist with calculations) and you’ll use it to understand how a lot passion you are going to pay.

As an example, this is the desk for my April 2022 Collection I bond (set to $1,000):

If I redeem my bond, I give up the final 3 months (September, October, and November of 2023) – or $15.20.

If I had a $1,000 Bond issued in April 2022, the “Present Worth” in my desk of Present Holdings would display $1,108.80.

Must You Money Out Your Bonds?

You presently know all your bonds and learn how to glance up their mounted charges. You can also see their present rate of interest in addition to how a lot passion you’d give up in case you redeem it inside 5 years of factor.

For me, the verdict tree seems like this:

- In case you are out of doors of the 5 yr penalty duration, test your charges towards what you’ll get from a 12-month certificates of deposit (recently within the mid-5%). Likelihood is that you’ll money out, stick your cash in a CD, and earn extra with larger flexibility. Even with Collection I bond passion being exempt from state and native taxes, the CDs would possibly nonetheless be a greater charge.

- In case you are inside the 1 yr no withdrawal, no resolution to be made right here!

- For everybody else in between, that’s the tricky number of whether or not you wish to have to stay your bonds or redeem them. You give up the final 3 months of passion in case you redeem.

I set the bar for whether or not I will have to redeem my bonds at the most productive rate of interest for a 12-month CD. That’s my private bar. I believe that given the present charge setting, if it’s now not beating a 12-month CD, it’s time to transport on. I set it there for the reason that 12-month charge isn’t the very best charge available in the market. You’ll be able to get the next menace unfastened charge simply from different Treasuries (test the newest public sale charges).

Test the mounted charge. Many people are keeping Collection I bonds with a zero.00% mounted charge (set in Would possibly 2020 and stayed there till it was once higher on November 2022). Test how a lot passion you’d be surrendering by way of redeeming at the moment (from the web page above) and notice whether or not you’ll do higher with an alternate (chances are high that you almost certainly can).

The inflation charge has been below 2% since Would possibly 2023. This implies a bond with a zero% mounted charge and a 2% inflation charge is now best getting you 4%. That’s a a long way cry from the 5%+ you’ll get in other places. And because you’ve been getting not up to 4% passion for rather a while… it’s a secure time to redeem.

In the end, one possibility is to redeem the 0% mounted charge Collection I bonds now and “turn” them (as much as the $10,000 annual in step with particular person most) into new Collection I bonds with the next mounted charge. November 2023 Collection I bonds have a hard and fast charge of one.30% and a combined charge of five.27% so the ones generally is a excellent possibility for other folks in prime tax states.

As all the time, there are all the time particular instances. If you are expecting upper schooling bills, the passion from Collection I bonds may also be exempt from federal source of revenue taxes. If you realize you’ll be spending it there, it would make sense to stay keeping them.

What I Am Doing With My Collection I Bonds

Right here’s what I’ll be doing with my 4 bonds, proven above:

| Bond # | Factor Date | Pastime Price |

Mounted Price |

What I’m Doing |

|---|---|---|---|---|

| IAAAE | 04-01-2022 | 3.38% | 0.00% | Redeem |

| IAAAD | 11-01-2021 | 3.94% | 0.00% | Redeem |

| IAAAC | 10-01-2011 | 3.38% | 0.00% | Redeem |

| IAAAA | 10-01-2005 | 4.60% | 1.00% | Redeem |

For the primary 3 bonds, we’re inside 5 years so I can give up 3 months of passion however with a zero.00% mounted charge, our 3 months of misplaced passion shall be at a relatively low charge.

(as we noticed within the desk above, it’s $15.20 on a $1,000 bond or 1.52% for latest bond)

For the fourth bond (IAAAA), it’s past the 5 years so I surrender not anything (it’s additionally best valued at $100). The one hesitation comes from the mounted charge however it’s 1.20% – I will be able to get a brand new bond with a 1.30% mounted charge.

In the end, the one factor I surrender is that I will be able to best put $10,000 right into a Collection I Bond every yr (the entire of those 4 bonds is a long way better).

However with risk-free rates of interest out of doors of Collection I Bonds at such favorable charges, the restrict has no monetary affect.

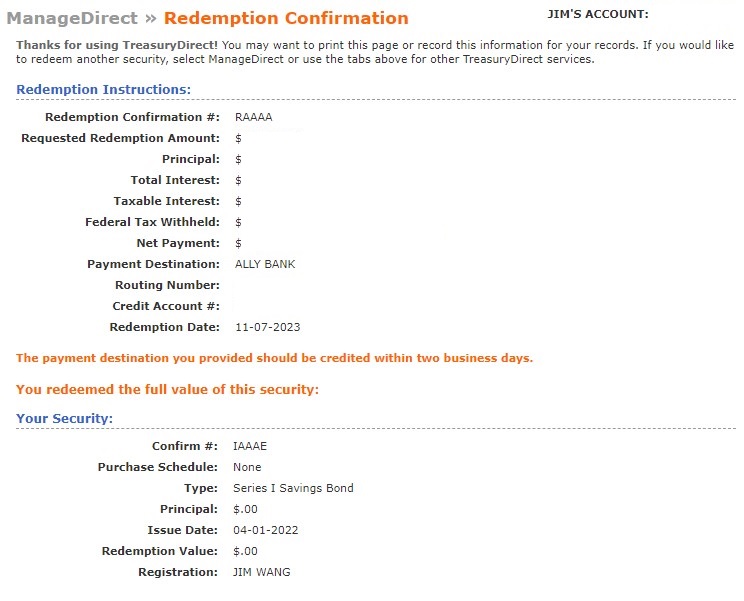

Learn how to Redeem Your Bonds

To redeem your bonds, merely return to the Present Holdings web page >> Element and click on Redeem.

You’ll be able to make a choice to redeem all or best a part of your bond (minimal of $25), one of the vital advantages of digital bonds!

Afterwards, you’re proven one affirmation web page after which the redemption is entire.

Simple as that!

What is going to you be doing?

[ad_2]