")

")

[ad_1]

This remark from the Fed is vintage Fed at paintings.

The Fed has no longer helped its personal purpose right here, as Austan Goolsbee, president and CEO of the Federal Reserve Financial institution of Chicago, stated in a speech remaining week: “I’m nonetheless seeking to procedure why long-end rates of interest are expanding.”

My solution: “Prevent speaking about elevating price at this level with a hawkish outlook!”

The Fed has expressed that actual yields, which means the place inflation is lately and the place charges are, are restrictive to the financial system, so sounding hawkish on financial coverage at this level can lead the bond marketplace to move upper greater than the Fed would love. Land the airplane, other people, land the airplane!

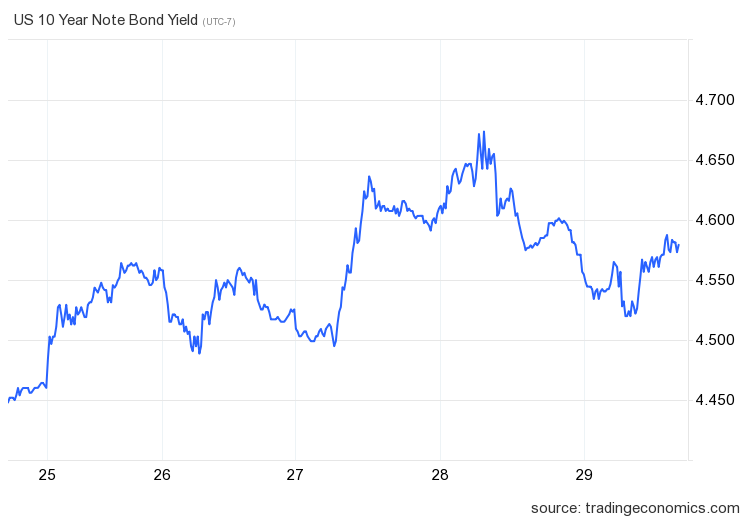

As you’ll see within the chart underneath, it was once every other wild week within the bond marketplace. Loan charges went from 7.39% to a top of 7.65% and ended the week at 7.44%. Prior to remaining week the top for loan charges this 12 months was once 7.49%.

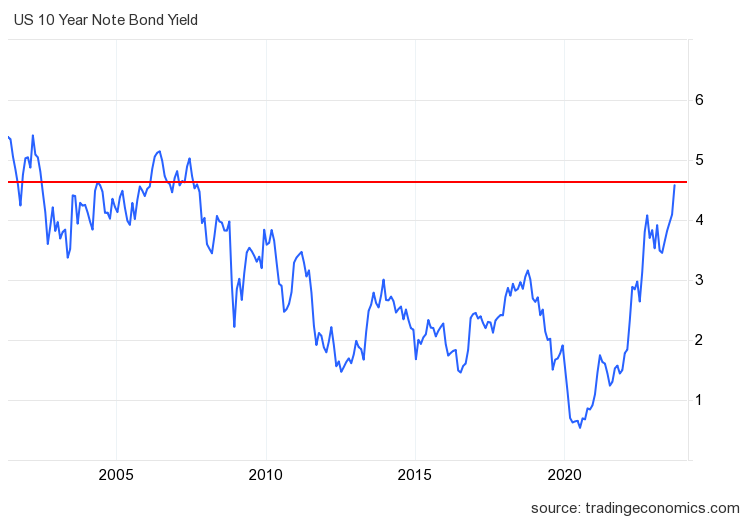

The bond marketplace has been risky, however after the 10-year yield broke the 4.34% degree, I’m gazing for the 4.63% degree. A detailed above that and follow-through bond marketplace promoting may just result in upper loan charges. Optimistically, the remaining two weeks stuck the Fed’s consideration. In the event that they cared a couple of comfortable touchdown, which I’ve been skeptical about from the beginning, as I mentioned right here on CNBC, the Fed could be extra aware of what they are saying and do.

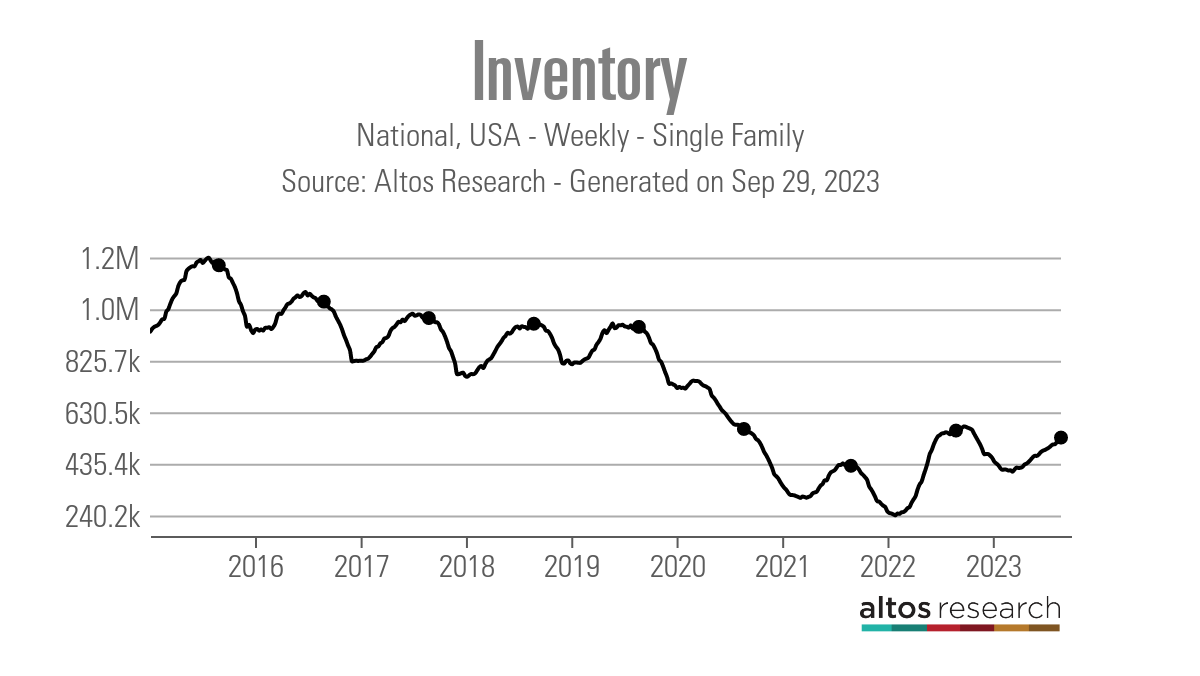

Weekly housing stock knowledge

Some of the issues I were given fallacious this 12 months is that I thought if loan charges stayed upper for longer, energetic stock would develop between 11,000 and 17,000 for no less than one of the crucial weeks; that hasn’t took place just lately with upper charges — shut however no cigar. T

Remaining week, the expansion of energetic listings slowed to 6,808. Seasonality is kicking in now, however we will have to be capable to proceed rising housing stock like we did remaining 12 months, as upper charges sluggish gross sales down, preserving houses in the marketplace longer.

Remaining 12 months, the seasonal top was once Oct. 28. Remaining week, in keeping with Altos Analysis:

- Weekly stock alternate (Sept.22-29): Stock rose from 527,938 to 534,746

- Similar week remaining 12 months (Sept. 23-30): Stock rose from 556,865 to 561,229

- The stock backside for 2022 was once 240,194

- The stock top for 2023 thus far is 534,746

- For context, energetic listings for this week in 2015 had been 1,187,2000

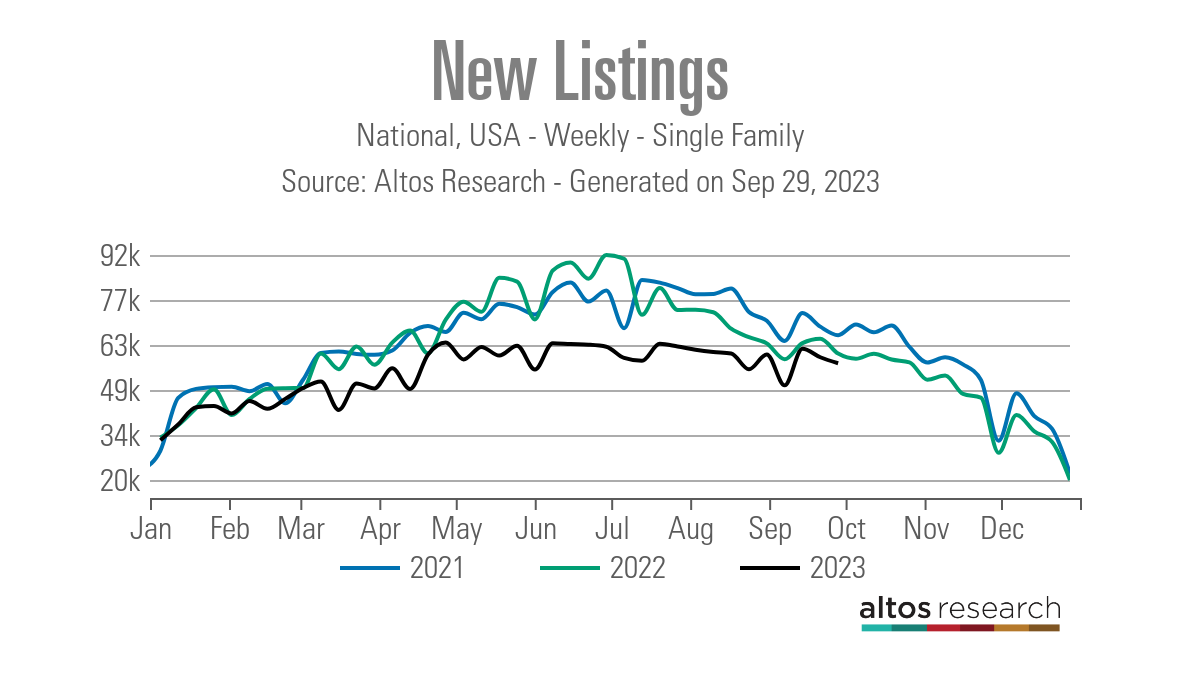

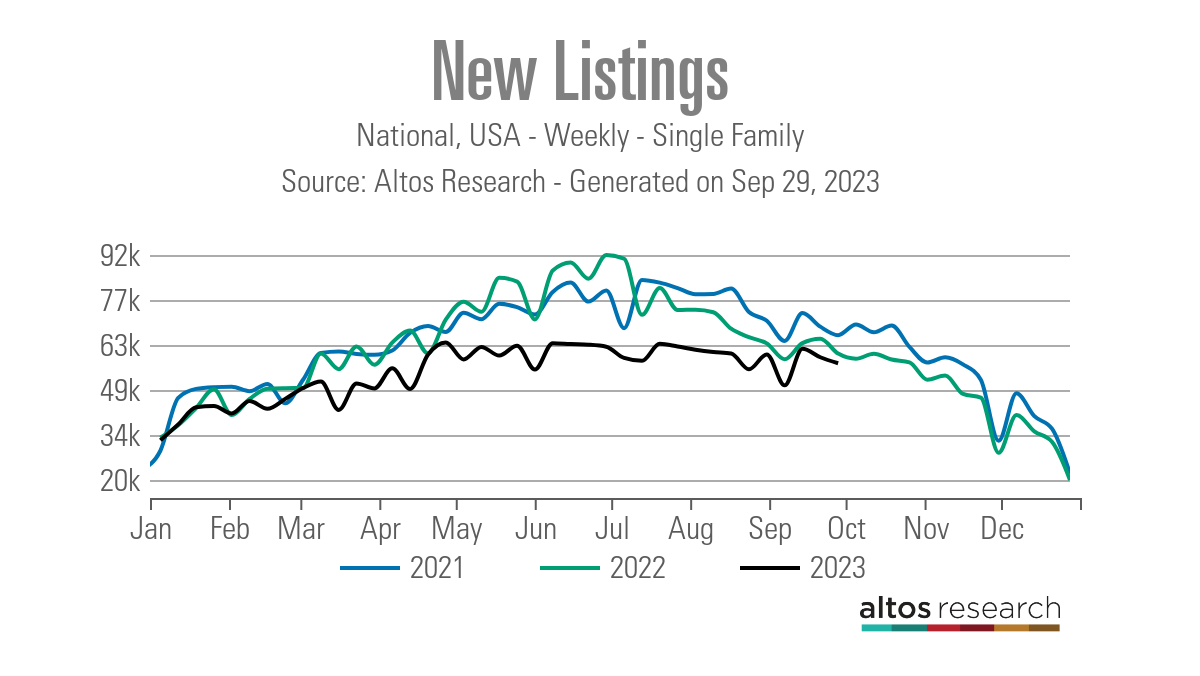

After some risky weeks with the brand new listings knowledge, issues glance very similar to previous within the 12 months once we had an orderly seasonal decline in new listings knowledge, which has been trending on the lowest ranges ever for over 13 months. Even with charges spiking, the brand new record knowledge hasn’t created every other new leg decrease. That is vital, as I be expecting flat to somewhat sure knowledge quickly because of a shallow bar.

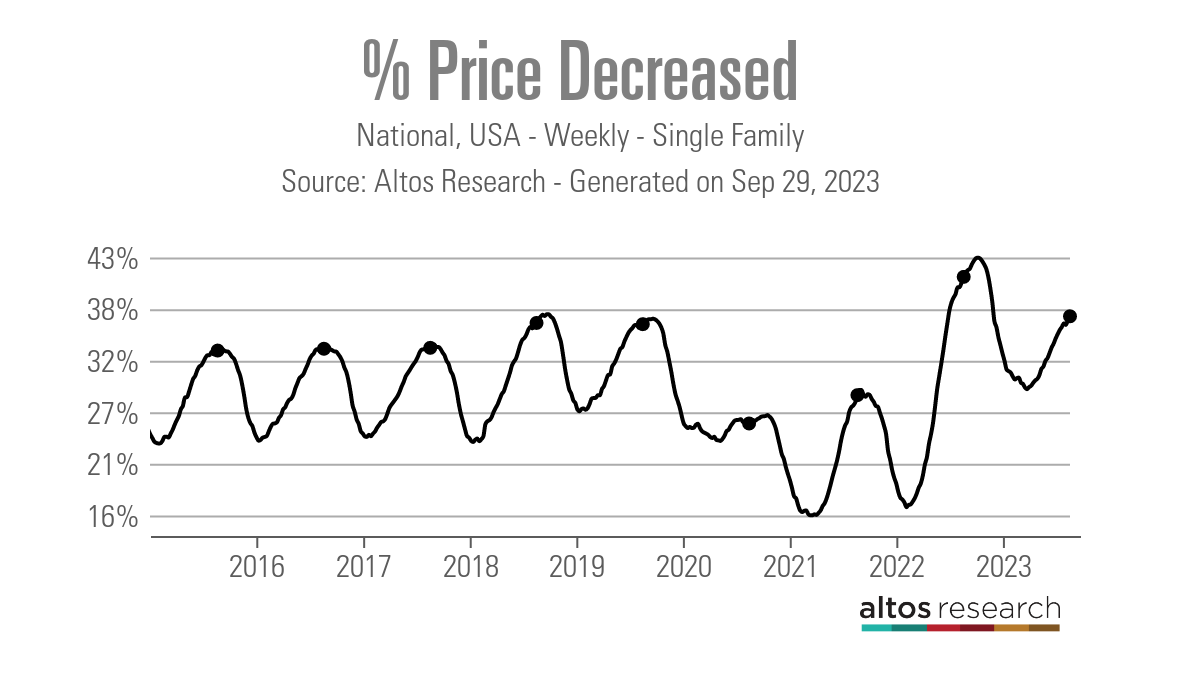

Traditionally, one-third of all houses have worth cuts annually. Remaining week’s worth cuts had been less than remaining 12 months on the similar time by way of 4%. This is occurring even with charges over 7% and a part of the reason being that housing stock has been unfavorable 12 months over 12 months since mid-June. As loan charges transfer upper, the share of worth cuts can develop however it’s trailing remaining 12 months’s proportion as house gross sales aren’t crashing like they did remaining 12 months.

Worth cuts for remaining week through the years:

- 2021: 29%

- 2022: 42%

- 2023: 38%

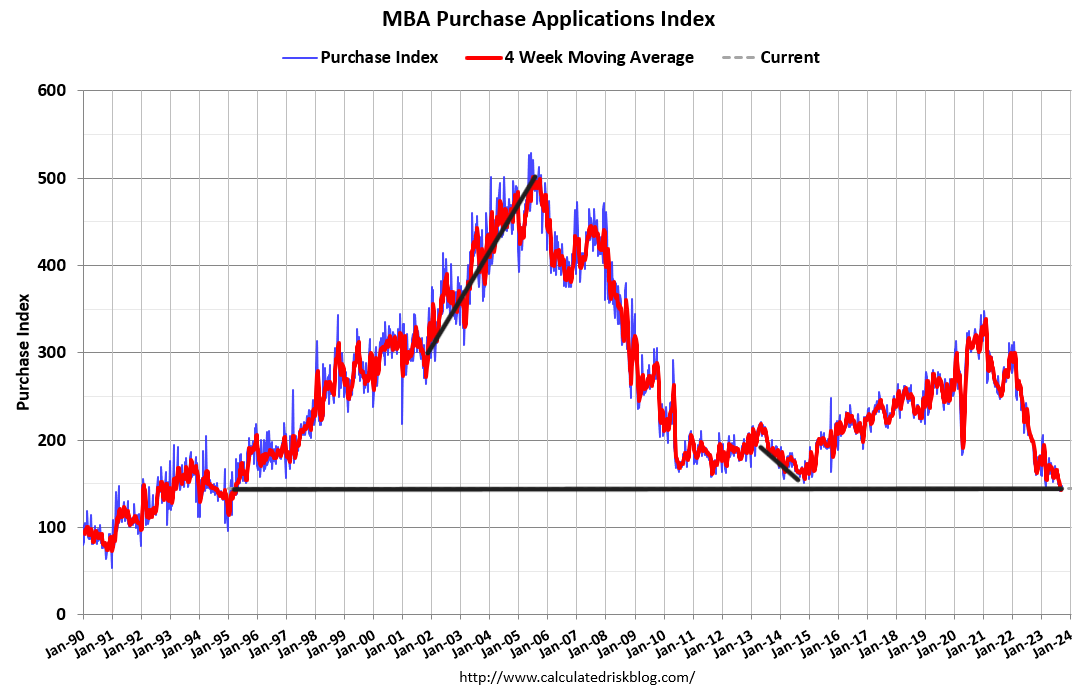

Acquire utility knowledge

Acquire utility knowledge was once 2% decrease remaining week as opposed to the former week, making the year-to-date depend 17 sure prints, 19 unfavorable prints, and one flat week. If we begin from Nov. 9, 2022, it’s been 24 sure prints as opposed to 19 unfavorable prints and one flat week. The week-to-week knowledge has gotten softer since loan charges were trending above 7%. On the other hand, it’s no longer crashing like remaining 12 months as a result of we’re running from a decrease bar.

The week forward: It’s jobs week! (If the federal government is open)

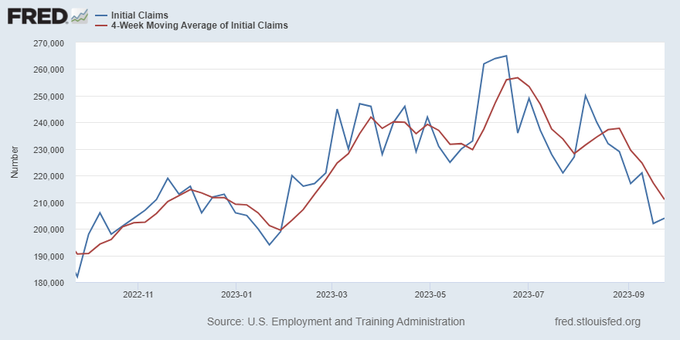

If we don’t have a govt shutdown, the week forward will probably be jobs week once more! The Fed was once satisfied about exertions knowledge remaining month as task openings were falling, and the task expansion knowledge is cooling down. On the other hand, jobless claims are nonetheless going sturdy, so they’ve extra paintings to do in attacking the exertions provide. Along with jobless claims, this week we will be able to even have task openings, the ADP jobs record, and the BLS Jobs Friday record, which might transfer the bond marketplace this week.

Additionally, I will be able to watch this week to look if extra Fed participants remark about emerging long-term charges. The Fed wish to stay charges upper for longer, but when the bond marketplace will get a whiff of any horrible recession knowledge, it’s going to take yields down. To this point, jobless claims knowledge hasn’t given them any explanation why to take action.

[ad_2]