[ad_1]

The trade has regained its production tempo, however

attainable disruptions in chip provide stay, and manufacturing

momentum disruption has driven a 100-million-unit 12 months into the

subsequent decade.

The affect of the COVID-19 pandemic at the availability of

semiconductor chips took a drastic toll on all aspects of the

automobile trade, and in flip the worldwide economic system. However in

mid-2023, the worst of the fallout turns out to have settled, and the

auto trade has discovered a brand new customary. In brief, the shortage of

provide of semiconductor chips that hobbled car manufacturing for

maximum of 2021 and 2022 has light into the background — with some

exceptions — in step with contemporary research through S&P International

Mobility.

S&P International Mobility estimates that during 2021 greater than 9.5

million gadgets of worldwide light-vehicle manufacturing used to be misplaced as a

direct results of a loss of vital semiconductors, with the 3rd

quarter of 2021 experiencing the biggest affect with an estimated

quantity lack of 3.5 million gadgets. Some other 3 million gadgets have been

impacted in 2022. (Those losses are estimated from inspecting

authentic apparatus producer bulletins, in comparison to S&P

International Mobility’s estimate of manufacturing making plans volumes all through

the similar <span/>timeframes.)

All over the primary part of 2023, alternatively, losses identifiable as

particularly associated with the semiconductor scarcity fell to about

524,000 gadgets globally. Even if the availability of semiconductors

stays constrained, extra predictable availability has allowed

automakers to conform their manufacturing schedules.

In consequence, we see semiconductors as a selected explanation for

manufacturing disruptions taking place with much less frequency.

Manufacturing in 2023 has stepped forward as automakers and providers have

tailored to the present setting, and 2023 gross sales are bettering

with extra stock. That mentioned, the pre-pandemic momentum towards a

100-million international car manufacturing 12 months has been set again through a

decade, in step with S&P International Mobility research.

So, the place are we in mid-2023?

To level-set expectancies, previous to the pandemic there at all times

have been semiconductor provide chain demanding situations — however they tended to

be episodic, impacting a unmarried part kind or particular person

provider<span/>. The

semiconductor providers have customer support and manufacturing

readiness groups operating at the back of the scenes, and those assets have

at all times controlled a lot of these shortages with most effective uncommon

interruptions in provider.

What used to be distinctive concerning the pandemic length used to be the wholesale

shortages amongst <span/>just about all providers,

impacting more than one part sorts (together with microcontroller gadgets

— or MCUs — and analog in line with mature procedure node

capability).

“We have now moved from glaring disruption, obviously visual on the

automaker and plant point, to a level the place we all know constraint

stays, however it’s unimaginable to spot,” mentioned Mark Fulthorpe,

S&P International Mobility government director of worldwide light-vehicle

manufacturing.

“We are actually able the place the car trade has tailored to

a constrained provide, and because of this is way much less more likely to be hit

through vital disruption,” Fulthorpe added. “With the present

semiconductor provide ranges, we estimate that 22 million gadgets of

international light-vehicle manufacturing in step with quarter might be

supported.”

On the other hand, trade call for for increasingly more advanced infotainment,

complex protection and car autonomy methods will proceed to

escalate utilization of semiconductors in cars. Phil Amsrud, senior

predominant analyst within the S&P International Mobility provider and

elements staff, estimates that the price of semiconductors

put in in cars averaged US$500 in step with automobile in 2020, however is

forecast to achieve US$1,400 in step with automobile through 2028.

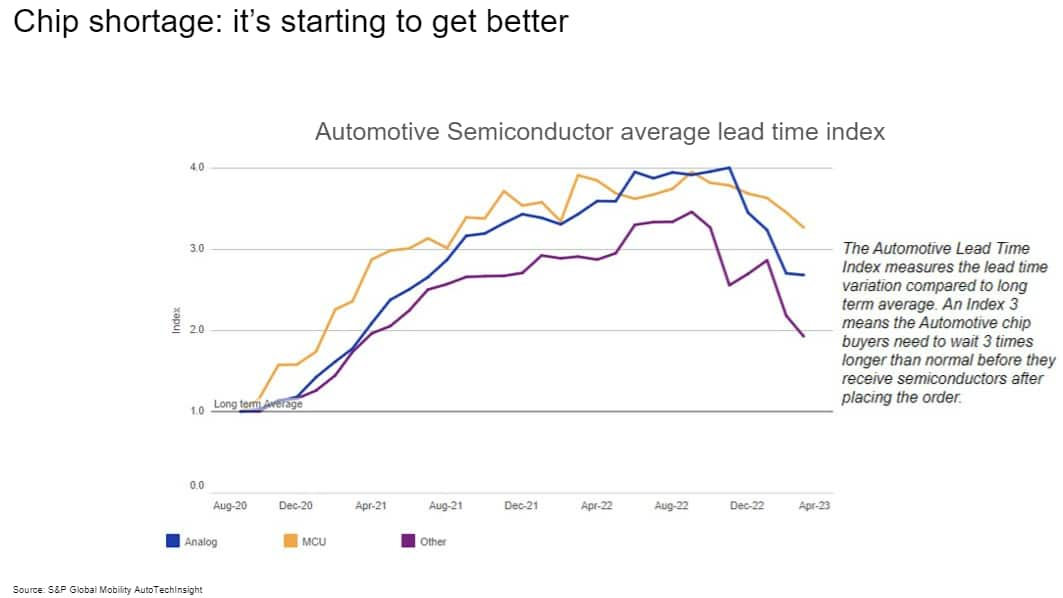

“Earlier than the pandemic, the lead time from order to cargo of

chips used to be 3 to 4 months. All over the pandemic in 2021 and

2022, that wait grew to a 12 months or longer,” Amsrud mentioned. “However whilst

different industries — corresponding to cell phones and <span/>PCs — have

skilled cooling call for of past due,

automobile semiconductor call for is expanding, and a few chip

producers have pivoted capability to deal with that want.”

That mentioned, the forms of chips for automotive-grade use as opposed to

communications apparatus ceaselessly aren’t the similar; or there are

other qualification ranges in automobile that complicate the usage of

shopper grade elements in automobile programs, Amsrud

famous.

Possible for long run disruption

Even if the semiconductor disaster is <span/>in large part resolved, the chip provide

state of affairs nonetheless carries a point of uncertainty. Call for nonetheless

exceeds provide of a number of chip sorts. There’s a scarcity, whilst

the car trade can higher arrange it lately than two years in the past.

Power at the provide chain stays with <span/>possibility of additional disruption.

Whilst call for for chips from the shopper electronics trade

has softened not too long ago, it’s more likely to rebound whilst the usage of

semiconductors in vehicles continues to extend, which might be components

indicating persisted power. In the meantime, the structural loss of

capability for mature node capability has now not been addressed.

Geopolitical industry dangers stay as neatly, as evidenced through mainland

China’s resolution in early July to limit exports of a few key

semiconductor fabrics. Business tensions between the <span/>US and mainland China

stay excessive, and the semiconductor provide can nonetheless be suffering from

long run strikes from all sides.

Consolidation of electronics in automobiles may be using the

automobile semiconductor call for, with

area controllers and central computer systems changing electronics

regulate gadgets (ECUs). This doesn’t reduce the desire for chips,

however quite method extra — and extra robust — chips are

wanted.

The excellent news is that this consolidation permits the usage of extra

complex system-on-chip (SoC) and discrete reminiscence, which might be

processed at extra complex procedure nodes. That is the place maximum

capability funding goes. The <span/>dangerous information is a few analog, discrete and

energy elements will at all times be on mature procedure nodes, which

obtain a lot much less funding. The motion to area controllers

and central computer systems would possibly cut back the selection of modules in step with car

and can alternate the combo of semiconductors however it is going to now not cut back

the total selection of semiconductors. Analog, discrete and tool

gadgets gets little if any take pleasure in transferring to complex

procedure nodes.

There is also the query of the way <span/>OEMs method the producing capability

equation, following two years of decrease volumes however — in some

circumstances — more potent earnings. Confronted with decrease capability, <span/>in large part because of the chip

disaster, automakers have been ready to command larger pricing, closely

cut back reliance on incentives, and allocate chips to higher-margin

merchandise and trim ranges inside of product strains.

For the ones automakers, there is also a reconsider on easy methods to arrange

the stock as opposed to call for, and incentive to strengthen the pricing

energy with controlled manufacturing and to proceed allocating chips to

high-margin, high-feature set cars that inherently additionally require

extra chips. <span/>Taking a look

ahead, the query would possibly not merely be what number of chips are

to be had to the automobile trade, however how other automakers

allocate their provide.

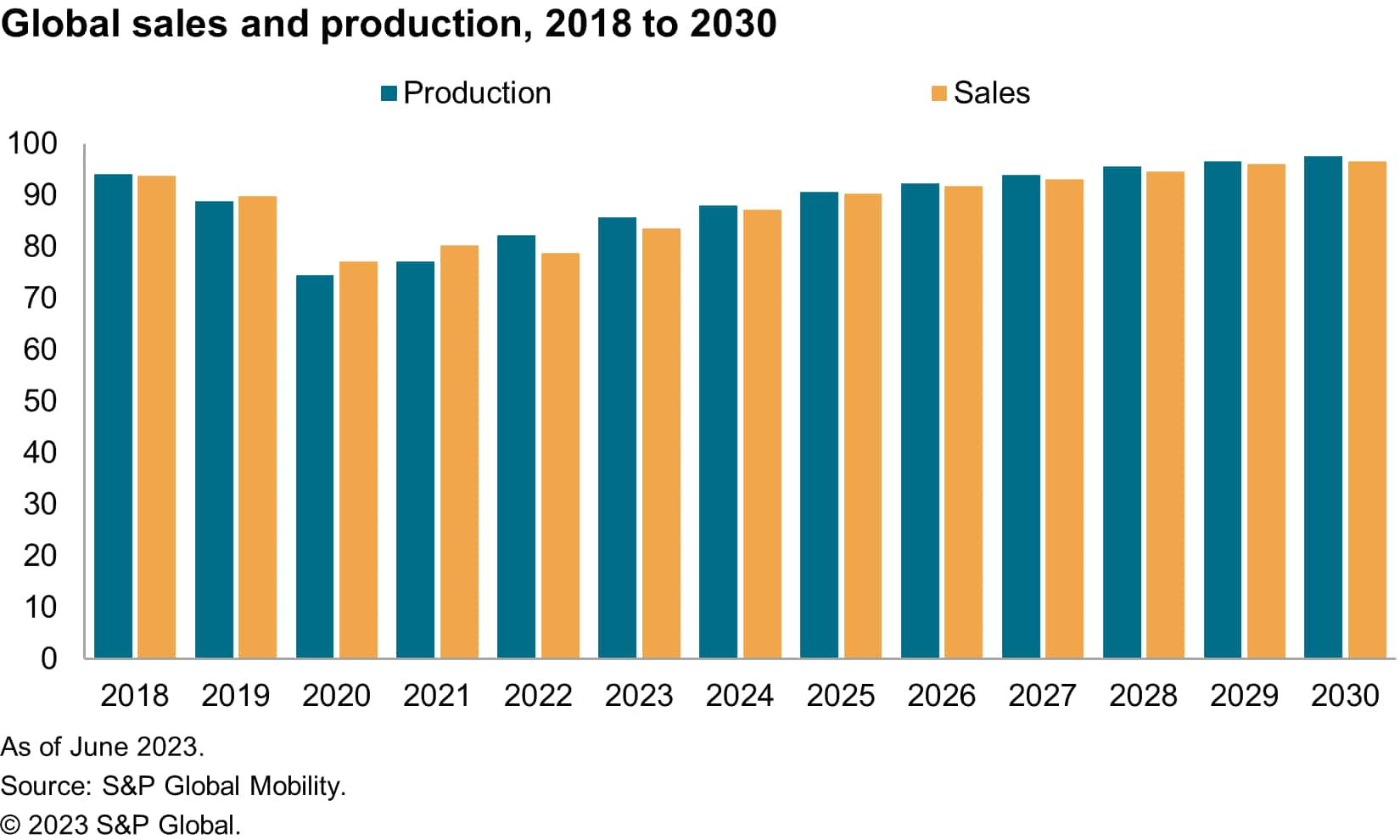

Trade trajectory set again through a decade

Whilst manufacturing and gross sales are bettering, and semiconductor

provide is not anticipated to be a supply of disruption for

car manufacturing, there may be little likelihood to “make up” the misplaced

manufacturing or gross sales from 2020 thru 2022. The early-2019 S&P

International Mobility forecast — issued previous to the COVID-19

pandemic and the next shutdowns — anticipated each international

gross sales and manufacturing to exceed 100 million gadgets once a year as quickly

as 2022.

That milestone is no longer anticipated till previous 2030, in step with

our research, demonstrating that the car trade’s expansion

trajectory has been thrown off through <span/>more or less a decade in comparison with

pre-pandemic expectancies. The semiconductor disaster used to be a number of the

maximum disruptive of a number of exterior affects that mixed to force

down the alternatives anticipated in 2019, however not at all the one

one.

International light-vehicle gross sales reached 93.8 million gadgets in 2018.

A number of components led to gross sales to drop in 2019, after which COVID-19 and

related affects ended in a 14% year-over-year decline in international

auto gross sales in 2020. The restoration in 2021 used to be held down through

manufacturing constraints quite than through a loss of shopper call for or

willingness to shop for, and in 2022, the ones constraints led to but

some other decline.

The June 2023 S&P International Mobility forecast sees gross sales

achieving 83.6 million gadgets globally this 12 months — some other

93-million-unit 12 months isn’t forecast till 2027, thus pushing the

attainable for gross sales above 100 million gadgets previous 2030.

As for international light-vehicle manufacturing, that quantity reached 94.1

million gadgets in 2018, additionally falling in 2019 to about 88 million.

The pandemic and comparable provide chain woes pulled manufacturing down

through 16% 12 months over 12 months in 2020. With provide chain problems coming near

a extra normalized state of affairs in 2023, output is forecast to achieve

85.6 million gadgets this 12 months. Even if we will be able to see some other

88-million-unit manufacturing 12 months in 2024, output above 94 million

gadgets isn’t anticipated to happen till 2028.

Mid-2023 marks an inflection level when the semiconductor provide

is not proscribing car manufacturing. There’ll proceed to be

portions of the availability chain that pose threats however the ones appear extra

episodic than systemic. Geopolitical threats persist relating to

wafer and packaging capability within the Asia-Pacific area, however the

trade may be transferring ahead with including capability in Japan,

Europe, and North The united states.

The effectiveness of and responses to the US-led semiconductor

era embargo are nonetheless to be made up our minds. Rebounds in

non-automotive semiconductor marketplace expansion are an unknown issue.

From the automobile trade point of view, classes realized from the

pandemic shortages — particularly the long-term steadiness of mature

as opposed to complex procedure nodes — is significant. The developments of

electrification and independent using will affect car

architectures, which in flip will affect the combo and selection of

semiconductors used. The trade will have survived the COVID

semiconductor disaster, however that doesn’t imply it’s out of the

woods.

MOBILE PHONE DEMAND COOLS; AUTO CHIPS RED HOT

AUTOMOTIVE COMPONENT FORECASTS

DOMAIN CONTROLLERS AND ZONAL ARCHITECTURE

AUTOMOTIVE TECHNOLOGY MARKET RESEARCH AND ANALYSIS

LIGHT VEHICLE PRODUCTION FORECASTS

This text used to be printed through S&P International Mobility and now not through S&P International Rankings, which is a one by one controlled department of S&P International.

[ad_2]